When Full Coverage Stops Making Sense

You just got your renewal notice. Same coverage, higher premium, no explanation. The car is paid off, you drive 4,000 miles a year, and you're wondering whether you're paying for collision and comprehensive coverage you don't need anymore. Your neighbor dropped both on their 12-year-old sedan and their premium dropped by half. Your agent says most seniors keep full coverage. You want to know what actually makes sense for your situation.

The paid-off vehicle changes the math, but not in the direction most insurance content suggests. Collision coverage pays you what your car is worth today after a wreck. Comprehensive pays for theft, weather damage, and vandalism. Neither cares whether you still owe the bank. The question isn't whether the lien is gone — it's whether the payout would exceed what you'd lose by self-insuring the replacement cost.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteBodily Injury Minimum Per Person

$25,000

Most state minimums were set decades ago and haven't kept pace with medical costs or the asset exposure retirees face in at-fault accidents. Your retirement accounts, home equity, and savings are all exposed above the liability limit.

State insurance regulations, various jurisdictions

The Collision Coverage Decision

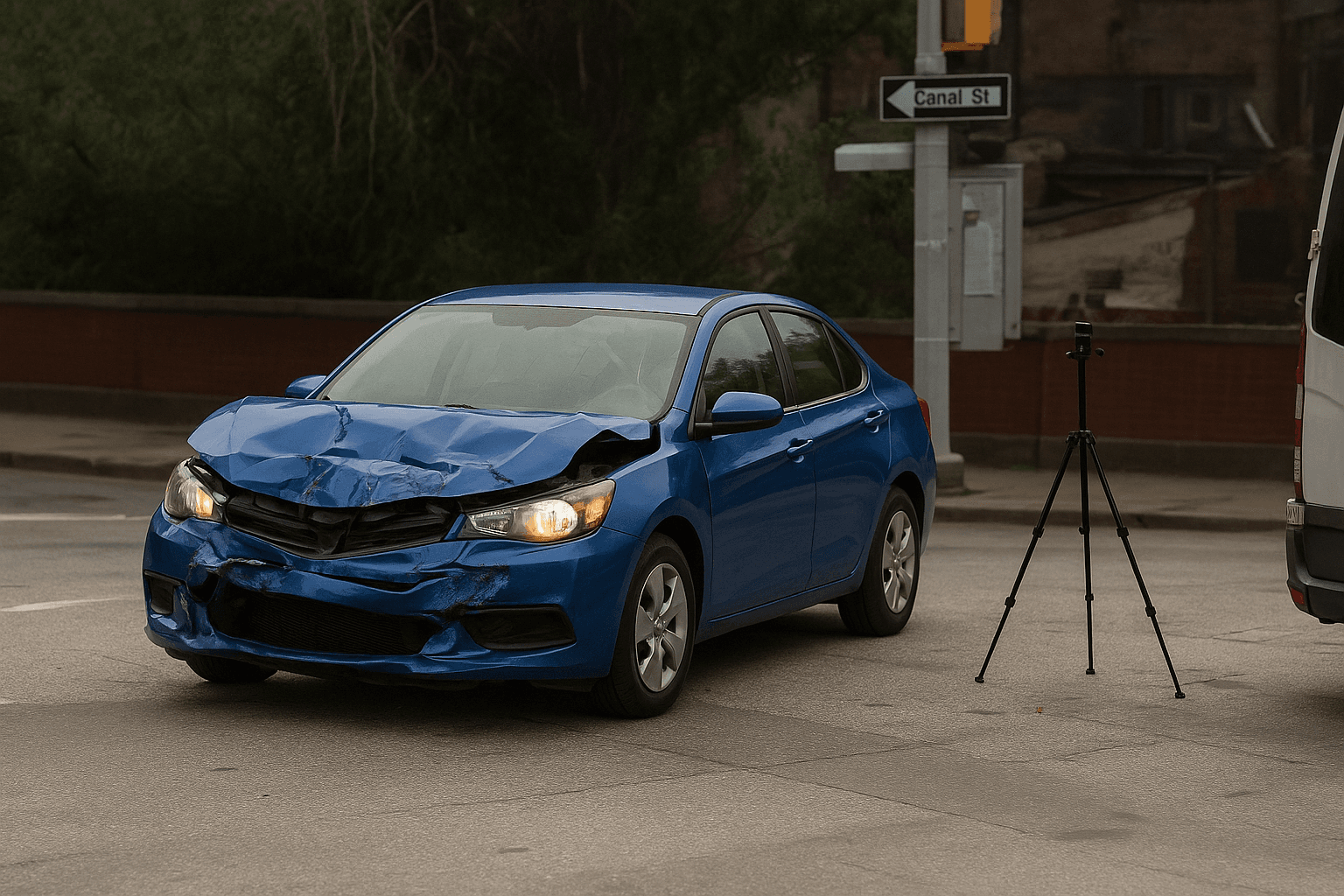

Collision coverage pays the actual cash value of your vehicle after depreciation, minus your deductible, if you cause an accident or hit an object. On a paid-off car worth $6,000, a $500 deductible means the maximum payout is $5,500. If your annual collision premium is $400, you recover your premium in roughly 14 years of no-fault accidents. That's the actuarial frame.

The household frame is different. Can you replace the car tomorrow without the insurance payout? If you have $6,000 in accessible savings earmarked for vehicle replacement and losing the car wouldn't force you into debt or a hasty purchase, self-insuring collision makes sense. If that $6,000 would come from an emergency fund you cannot afford to drain, keep the coverage.

Most senior drivers fall between those poles. The car is worth more than pocket change but less than the cost of disrupting retirement cash flow. The judgment call: would the premium savings over three years equal or exceed the vehicle's current value? If yes, redirect the premium to a vehicle replacement fund and drop collision. If no, the coverage is cheaper than the exposure.

Collision coverage stops at actual cash value. A 10-year-old car depreciates faster than you'd expect, and the payout reflects what a buyer would pay today, not what replacement will cost you.

Comprehensive Coverage and Asset Age

On older vehicles, comprehensive often costs $150 to $300 annually with a $500 deductible. The math is simpler than collision: if your car is worth $4,000 and comprehensive costs $200 per year, one total-loss event every 20 years justifies the premium. Hail happens. Deer happen. Catalytic converter theft happens, and comprehensive is the only coverage that pays for it.

The coverage-fit question: do you park in a garage, live in a low-theft area, and drive routes with minimal wildlife? If all three are true and the vehicle is worth under $5,000, dropping comprehensive makes sense. If any one is false, or the car is worth more than $5,000, keep it. Comprehensive is cheap relative to the exposure it removes.

Related Articles

Liability Limits and Retirement Assets

Liability coverage is not optional. Collision and comprehensive protect your car; liability protects everything else you own. If you cause an accident that injures someone, the other driver's medical bills, lost wages, and pain-and-suffering claim come out of your liability limit first, then out of your assets if the judgment exceeds your coverage.

State minimums were written decades ago. A $25,000 bodily injury limit per person sounds adequate until you're sitting across from an attorney explaining that the other driver's hospital stay alone was $90,000. Your home, your retirement accounts, your savings — all exposed above the limit. Most financial planners recommend liability limits equal to your net worth, and umbrella policies for exposure above $500,000.

Senior drivers on fixed incomes often reduce the wrong coverage. Dropping collision on a $4,000 car makes sense. Carrying minimum liability when you own a paid-off home and have $300,000 in retirement savings does not. Liability premiums scale slowly with higher limits; doubling your coverage from $50,000 to $100,000 per person typically adds $60 to $120 annually. The asset protection is worth more than the premium.

State Mature-Driver Discount Floor

10%

Many states mandate insurers offer a discount to seniors who complete an approved defensive driving course. The statutory floor is the minimum; carriers may exceed it. The discount applies only when you submit the certificate and expires when the certificate does, typically every three years.

State insurance statutes, various jurisdictions with mature-driver discount mandates

The Mature-Driver Discount Renewal Gap

You completed the defensive driving course three years ago. Your carrier applied a 10% discount at the next renewal. This year, your premium increased and you assumed it was the normal age-factor adjustment everyone talks about. It wasn't. The discount expired when your course certificate did, and your carrier removed it at renewal without telling you. Most insurers require a new certificate every three years to keep the discount active.

This is the gap competing articles never surface. Mature-driver discounts are not permanent. They attach to the certificate, not to your age or driving record. When the certificate lapses, the discount disappears. Your agent will not remind you. The renewal notice will not flag it. You'll see a rate increase and attribute it to actuarial age factors when the real cause is administrative: you didn't re-enroll in the course.

Check your current policy declarations page. If you see a mature-driver or defensive-driving discount line item, note the certificate date. If it's older than three years, the discount is gone at your next renewal unless you complete a new course before then. If you don't see the discount on your declarations page and you're over 55, ask your carrier whether they offer one and what course providers they accept. Many seniors qualify and never apply because no one told them the discount exists.

Medical Payments and Medicare Coordination

Medical payments coverage pays your medical bills after an accident regardless of fault, up to the policy limit. Medicare is primary for seniors over 65, meaning Medicare pays first and medical payments coverage pays secondary for expenses Medicare doesn't cover: deductibles, co-pays, and services outside Medicare's scope.

If you have comprehensive Medicare Supplement coverage, medical payments coverage duplicates what your Medigap plan already handles. Dropping it saves $40 to $80 annually with minimal exposure. If you have Original Medicare only, keeping $5,000 in medical payments coverage makes sense — it closes the gap Medicare leaves open for accident-related care. Personal injury protection works the same way in no-fault states; coordinate it with your health coverage, not your car's value.

What To Do Right Now

Pull your current policy declarations page and your most recent renewal notice. Check three things: the mature-driver discount line item and certificate date, your liability limits against your net worth, and your collision and comprehensive deductibles against your vehicle's actual cash value. If the mature-driver discount is missing or expired, enroll in an approved course before your next renewal. If your liability limits are below your assets, request quotes for $100,000/$300,000 or $250,000/$500,000 coverage.

If your car is paid off and worth under $5,000, request a quote with collision removed and compare the annual savings to the vehicle's replacement cost. If the savings exceed the car's value over three years, redirect the premium to a vehicle replacement fund and drop the coverage. If your car is worth more than $5,000 or you cannot self-insure the replacement, keep collision and adjust the deductible instead — raising it from $500 to $1,000 cuts the premium without removing the coverage.

Compare what your current carrier charges against what carriers known for senior-driver programs would quote for the same limits. Get quotes with your mature-driver discount applied, your actual annual mileage reported, and your liability limits raised to match your asset exposure. The paid-off car changes the collision math; it doesn't change the liability exposure or the discount mechanics. Fix both before your next renewal, not after.